Low Load Life Insurance

• Preserve more

• Control more

• Leave more

DESIGNED FOR:

- Families with estates over $20M

- Family offices and private wealth managers

- Business owners seeking liquidity and succession planning

- Clients utilizing advanced estate planning strategies such as ILITs, SLATs, GRATs, or dynasty trusts.

What is low load life insurance?

Low-load life insurance combines life insurance coverage with an investment component. The investment component can be managed by the individual themselves or by an investment advisor representative. This type of policy can offer a transparent pricing structure, eliminating fees such as sales loads, surrender charges*, and administration fees. Other costs and fees will still apply. This can make it an attractive option for consumers seeking cost-effective and value-maximizing insurance solutions.

KEY HIGHLIGHTS

Potential benefits

- Increased cash value accumulation: Lower fees can lead to a greater buildup of cash value over time.

- Investment options: Some products offer up to 140 investment options, including subaccounts that include sectors such as equities, bonds, real estate, energy and infrastructure.

- Daily policy performance tracking: Policyholders can monitor their investments daily.

- Flexibility: The absence of surrender charges* can allow for easy access to account values, enhancing liquidity.

- Tax benefits: Policies offer tax-deferred growth on the account value during the lifetime of the policyowner, and the death benefit is income tax-free.

Potential downsides

- Investment risk: The cash value is invested in investment subaccounts. Returns are not guaranteed, and policy values will increase or decrease based on market performance.

- No guaranteed cash value: This insurance does not provide guaranteed cash value accumulation; all growth depends on market performance.

- Suitability considerations: Generally designed for clients with long-term time horizons, higher income, and risk tolerance.

*There are no surrender charges upon full surrender of the policy; some vendors may charge fees on partial surrenders.

Insurance guarantees are subject to the claims-paying ability of the issuing insurance company. Investments in variable products involve market risk, including the possible loss of principal.

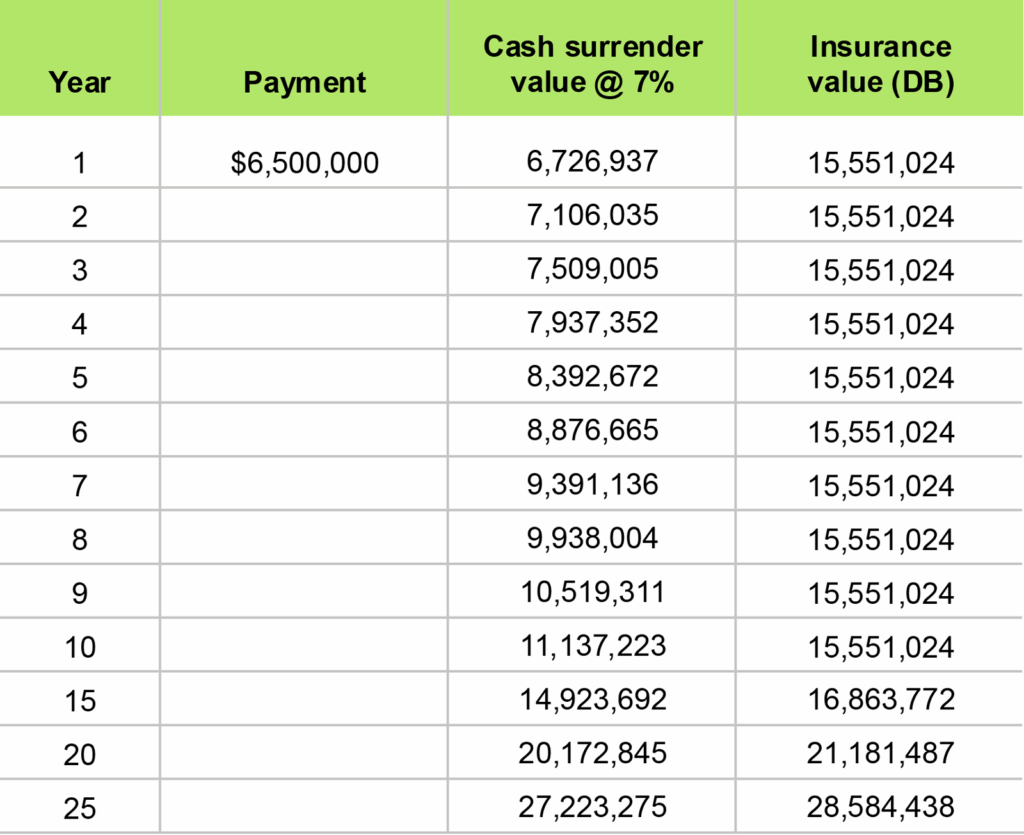

SAMPLE CASE: 25 YEARS

Client profile:

• C-suite executive• Male, age 57

• Health rating: Preferred, non-tobacco

Plan deposit:

$6,500,000

This example assumes a 7% rate of return in the investment subaccounts. For illustrative purposes only. Sample does not represent actual performance or guarantee future results.

How to manage the policy

The Investment portion of these policies can be managed by an investment advisor representative or the policy owner who may:

- Regularly review and adjust coverage based on life changes and financial goals.

- Stay informed about market trends to make strategic investment decisions.

- Work with an experienced insurance broker and your financial team to leverage available tools and resources to effectively manage the policy.

Tom Bishop will be acting as an Insurance Agent when selling this product and will not be providing ongoing investment management.

Integration into financial planning

Low load life insurance may be used as part of a comprehensive financial strategy. This type of policy is designed to provide a combination of tax-deferred investments and permanent insurance that can be strategically integrated into long-term financial plans.

Typically, assets are held in separate accounts, which helps protect them from the general creditors of the insurance company.

This insurance offers sophisticated investors a flexible, tax-efficient solution. By reducing certain traditional fees and granting access to a wide range of investment options, this product can help policyholders maximize savings and support long-term financial challenges such as liquidity, succession planning, estate planning, estate equalization, etc.

Client profile: Business owners

- Buy-sell funding … positively impact financial statements

- Executive compensation and retention plans

- Key person coverage

Client profile: High-net-worth families ($20M+)

- Family bank (lend money to family members)

- Existing life insurance policies (consolidation)

- Multi-generational wealth transfer

- Estate liquidity and asset protection

- Philanthropic/charitable legacy

Next steps

No follow-up will be made unless you request it—we respect your time and privacy.